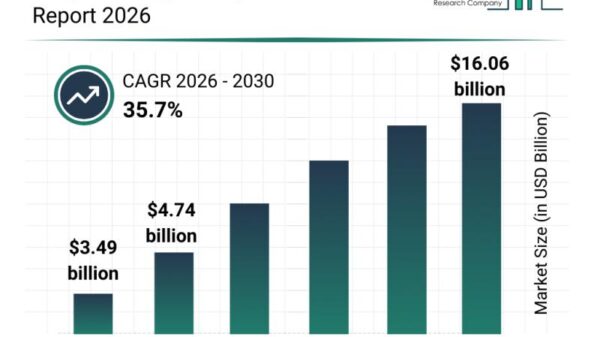

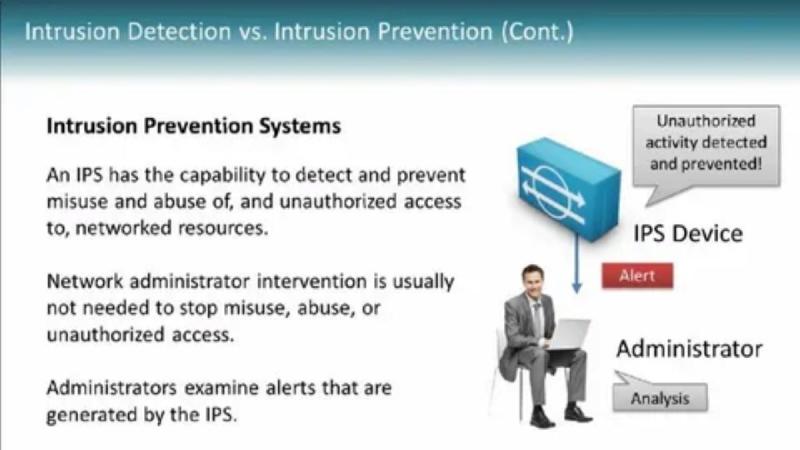

The global market for Physical Intrusion Detection and Prevention Systems (PIDPS) is expected to experience robust growth, expanding from an estimated value of US$ 14.8 billion in 2026 to US$ 24.6 billion by 2033, at a compound annual growth rate (CAGR) of 7.5% during the forecast period. This surge is largely driven by escalating security concerns across various sectors, prompting organizations to adopt advanced intrusion detection solutions.

Rising incidents of unauthorized access, theft, and vandalism have intensified the demand for PIDPS, with technologies incorporating artificial intelligence (AI), the Internet of Things (IoT), and real-time analytics significantly enhancing threat detection capabilities. Video surveillance systems continue to lead the adoption due to their ability to offer continuous monitoring and high-resolution imaging, making them crucial for effective threat identification.

In terms of end-users, the government sector is the largest segment, leveraging these systems for the protection of critical infrastructure. North America currently dominates the PIDPS market, accounting for an estimated 35% share, bolstered by stringent regulatory frameworks and substantial government investments in security technologies. Meanwhile, the Asia Pacific region is poised for the fastest growth, projected at a 11% CAGR, driven by rapid industrialization, urbanization, and increasing awareness of security measures in emerging economies.

According to market forecasts, hardware components are expected to capture a 55% market share by 2026, while services are anticipated to grow at the fastest rate, achieving a CAGR of 9.5% through 2033. Video surveillance systems are projected to command a 32% market share in 2026, while biometric systems are set to grow at a CAGR of 10.2% during the same period. The government sector is expected to represent approximately 28% of the market share by 2026.

The PIDPS market is segmented into hardware, software, and services, with hardware being the largest segment due to the widespread installation of surveillance cameras, sensors, and alarm systems in industrial, commercial, and residential facilities. Services are gaining traction due to the increasing need for managed security offerings, system maintenance, and consulting services.

Geographically, North America continues to lead, supported by advanced infrastructure, proactive cybersecurity policies, and high security awareness among organizations. Key industry players are heavily investing in AI-driven security solutions, reinforcing this dominance. In contrast, the Asia Pacific region is witnessing rapid growth, spurred by urban development and government initiatives focusing on smart city projects, with countries like China, India, and Japan making significant investments in physical security systems.

Market drivers include rising security concerns in critical sectors such as government, defense, banking, financial services, and industry, which have led organizations to adopt integrated and automated security systems. The increasing use of AI, IoT-enabled sensors, and real-time analytics enhances the accuracy and efficiency of intrusion detection systems, minimizing false alarms and operational risks.

However, the market faces challenges including high implementation costs associated with advanced AI-enabled systems, which may hinder adoption among small and medium-sized enterprises. Additionally, integration complexities with existing infrastructure and concerns over data privacy could slow the rate of adoption in certain areas.

Despite these challenges, opportunities abound, particularly in emerging economies where investments in physical security are on the rise. The trend towards smart cities, industrial automation, and cloud-based security solutions presents significant growth avenues for the PIDPS market. Moreover, technological innovations in video analytics, AI-driven threat detection, and biometrics offer promising prospects for solution providers looking to enhance their offerings.

Key players in the market include Honeywell International Inc., Johnson Controls International plc, Siemens AG, Bosch Security Systems, and ADT Inc., among others. Recent developments such as Honeywell’s launch of the 50 Series CCTV cameras, designed under the “Design in India, Make in India” initiative, and Johnson Controls’ partnership with AI analytics firms to integrate real-time threat detection into their systems highlight the industry’s focus on advancing security technologies.

The PIDPS market’s trajectory underscores the growing importance of security systems in an increasingly complex global landscape. As organizations prioritize safety and compliance, the evolution of these technologies will likely play a critical role in shaping future security strategies across sectors.

See also AI Agent Security Emerges as Critical Cyber Defense Frontier to Combat Evolving Threats

AI Agent Security Emerges as Critical Cyber Defense Frontier to Combat Evolving Threats AI-Directed Cyberattack by Chinese Hackers Targets 30 Firms, Reveals Anthropic Research

AI-Directed Cyberattack by Chinese Hackers Targets 30 Firms, Reveals Anthropic Research AI-Driven Cyberattacks Predicted to Surge in 2026, Warns Moody’s Report

AI-Driven Cyberattacks Predicted to Surge in 2026, Warns Moody’s Report AI-Generated Code Increases Debugging Time by 19% Amid Rising Silent Failures

AI-Generated Code Increases Debugging Time by 19% Amid Rising Silent Failures Recorded Future Reveals 87% of Firms Plan to Enhance Threat Intelligence Maturity by 2026

Recorded Future Reveals 87% of Firms Plan to Enhance Threat Intelligence Maturity by 2026