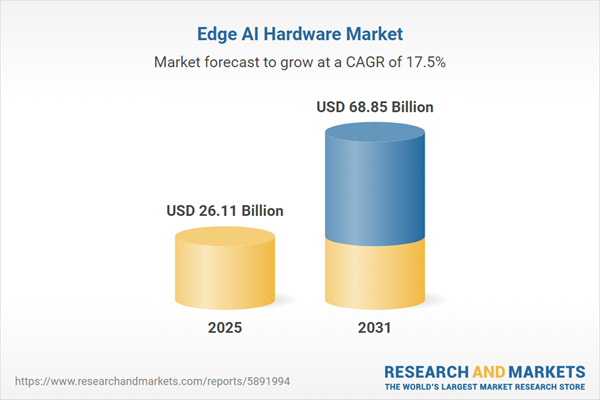

The Global Edge AI Hardware Market is projected to experience significant growth, with an expected increase from a valuation of USD 26.11 billion in 2025 to USD 68.85 billion by 2031, reflecting a compound annual growth rate (CAGR) of 17.54%. This surge is primarily driven by the proliferation of Internet of Things (IoT) devices and the rising demand for low-latency, on-device processing capabilities.

According to a recent report by ResearchAndMarkets.com, the Edge AI hardware sector incorporates specialized components like neural processing units (NPUs), graphics processing units (GPUs), and application-specific integrated circuits (ASICs). These technologies enable the execution of machine learning algorithms locally, reducing dependence on centralized cloud infrastructure. The increasing need for ultra-low latency in real-time decision-making processes and strict data privacy regulations further catalyze this shift towards robust, on-device processing.

However, the industry is grappling with significant challenges related to power efficiency. As manufacturers strive to integrate high-performance computing into resource-constrained devices, achieving a balance between performance and energy consumption proves difficult. The high computational demands for real-time AI inference often lead to rapid battery depletion, which is particularly problematic for devices used in remote industrial applications or wearable technology. This limitation may deter potential buyers from adopting intelligent edge solutions for mission-critical operations, thereby hindering broader market acceptance.

The urgency for hardware solutions is echoed by the ongoing rise in the number of connected endpoints. The Ericsson Mobility Report from June 2024 estimates that cellular IoT connections will reach approximately 4.5 billion by the end of 2025. Consequently, this trend necessitates the development of energy-efficient hardware capable of delivering high-performance inference at the network edge. In sectors like automotive and healthcare, where autonomous systems and AI integration are increasingly prevalent, the demand for specialized NPUs and GPUs that support advanced neural networks is escalating.

Recent statistics from the International Federation of Robotics (IFR) indicate that the global operational stock of industrial robots reached a record 4.28 million units in 2023. This growing base of intelligent automation highlights the increasing demand for computational resources that can handle complex tasks without relying on cloud connectivity. Memory bandwidth is becoming as critical as processing speed, with a 81.0% projected increase in the memory integrated circuit segment for 2024, according to the World Semiconductor Trade Statistics (WSTS). Such forecasts underscore the necessary infrastructure adjustments to support advanced AI workloads.

The integration of dedicated NPUs into mobile system-on-chip (SoC) architectures is revolutionizing consumer electronics. These advancements allow for sophisticated on-device inference, facilitating real-time language translation and image manipulation while reducing latency. Companies like Samsung Electronics have reported strong sales, particularly for AI-enabled flagship devices, indicating a rapid market shift towards hardware-supported intelligence.

Simultaneously, the adoption of Chiplet Technology and heterogeneous integration is transforming semiconductor design. This approach enables the combination of smaller, modular dies manufactured on different process nodes into a single package, allowing engineers to optimize performance and costs for specific AI workloads. According to TSMC, revenue from advanced packaging technologies is expected to exceed 10% of its total revenue in 2025, driven by sustained demand for high-performance computing solutions.

The Edge AI Hardware Market is expected to evolve with key players including Qualcomm Technologies, Inc., Huawei Technologies Co. Ltd., Samsung Electronics Co. Ltd., and NVIDIA Corporation. Each company is competing to enhance their offerings in a landscape marked by rapid technological advancement and changing consumer demands.

As industries increasingly adopt billions of sensors and smart connected devices, the imperative for efficient on-chip processing solutions will only intensify. The integration of AI into various sectors, from automotive to retail, reflects a broader shift towards decentralized computing architectures. Unless manufacturers can innovate to overcome the challenges associated with power efficiency, the massive ecosystem of IoT devices may not fully harness the potential benefits of edge AI, ultimately limiting the market’s growth potential.

With such dynamics at play, the Edge AI Hardware Market is poised for transformative change, promising to reshape how data is processed and utilized across various sectors in the coming years.

See also Neurophos Raises $110 Million to Advance Exaflop-Scale Photonic AI Chips for Data Centers

Neurophos Raises $110 Million to Advance Exaflop-Scale Photonic AI Chips for Data Centers Stanford HAI and Swiss National AI Institute Form Alliance for Human-Centered AI Research

Stanford HAI and Swiss National AI Institute Form Alliance for Human-Centered AI Research Intel Reports CPU Shortage to Peak in Q1 as AI Demand Surges, Hits $13.7B Revenue

Intel Reports CPU Shortage to Peak in Q1 as AI Demand Surges, Hits $13.7B Revenue CitiusTech and Ventra Health Launch vCision AI Platform to Boost Revenue Cycle Efficiency by 19%

CitiusTech and Ventra Health Launch vCision AI Platform to Boost Revenue Cycle Efficiency by 19%