Market analysts are revising their outlook on International Business Machines (IBM) as the company demonstrates accelerating financial performance and a strategic focus on monetizing advanced technologies. This shift towards software, hybrid cloud, and artificial intelligence is beginning to impact growth metrics, signaling a departure from the stagnation that characterized the past decade.

Recent upgrades from analysts reflect a more optimistic earnings forecast for IBM. Zacks Investment Research has elevated the company’s rating to Rank #2 (Buy), driven by substantial upward revisions in profit expectations. Analysts project earnings per share (EPS) for the current quarter to reach $4.33, marking a year-over-year increase of 10.5%. Furthermore, quarterly revenue is expected to hit $19.21 billion, an increase of 9.5%. For the full year, the consensus EPS estimate stands at $11.39, indicating a 10.3% rise, while revenue projections are set at $67.02 billion, representing a 6.8% increase.

This growth acceleration follows the spin-off of IBM’s managed infrastructure business into Kyndryl, allowing the company to sharpen its focus on core growth areas. Institutional investor Vista Investment Partners LLC notably increased its stake in IBM by over 862% during the third quarter, a move that signals strong confidence in the company’s strategic direction.

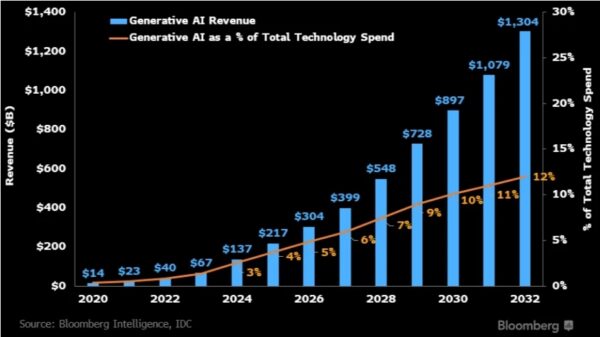

A critical component of IBM’s future growth lies in its ability to transform investments in artificial intelligence into consistent revenue streams. A recent report titled “AI Outlook 2026,” which focuses on the Asia-Pacific region, reveals a significant trend: approximately 64% of AI spending is now directed toward core business functions, rather than experimental pilot projects. This shift from testing to operational deployment positions AI as a direct contributor to revenue.

IBM’s watsonx platform is central to this transition, with key applications in sectors like banking for embedded financial solutions, as well as in industrial applications that utilize predictive maintenance automation. Successful scalable deployments in these areas are anticipated to drive meaningful growth in the coming years.

Alongside its AI initiatives, IBM is also advancing its quantum computing capabilities as a strategic differentiator. Market analyses indicate that IBM maintains a strong technological lead over smaller competitors, such as Rigetti Computing. The company is currently focused on its 120-qubit “Nighthawk” chip, which can process up to 5,000 two-qubit gates. The roadmap includes plans to increase this capacity to 10,000 gates by 2027, complemented by the development of a fault-tolerant quantum computer codenamed “Starling” by 2029. This long-term vision provides a stability buffer; unlike pure-play quantum firms, IBM’s investment case does not depend solely on the swift commercialization of quantum technology but rather enhances its established cloud and software offerings.

Financially, the market appears to be pricing in this growth trajectory with a premium. Zacks assigns IBM a Value Style Score of “D,” suggesting that shares are trading at a higher valuation than their historical averages. However, the company backs this up with strong profitability metrics, including a trailing twelve-month gross margin of 57.81%, significantly surpassing the sector median of approximately 49%.

IBM offers a different risk profile when compared to many high-beta technology stocks, combining moderate growth with more stable price movements. While speculative semiconductor equities often react sharply to market sentiment, IBM presents an appealing option for investors seeking AI exposure with potentially lower drawdown risks.

Technical indicators mirror this growing optimism as well. Shares closed Friday at $304.42, just below the 52-week high of $304.56. The stock has advanced approximately 42% year-to-date and remains well above its key moving averages, confirming the prevailing upward trend. The fundamental setup heading into the new year appears constructive, characterized by double-digit earnings growth, a clear roadmap for AI monetization, advancements in quantum computing, and robust profitability that justifies the current valuation premium.

The upcoming quarterly results will serve as a crucial test for IBM, particularly regarding revenue contributions from AI and hybrid cloud offerings, along with margin performance. Success in these areas would likely reinforce IBM’s position as a relatively defensive beneficiary of AI advancements as we approach 2026.

See also China Proposes New Rules for Human-Like AI, Mandating Ethical Use and Security Assessments

China Proposes New Rules for Human-Like AI, Mandating Ethical Use and Security Assessments Bosch Reveals AI Cockpit at CES 2026 with 200 TOPS Processing and Microsoft 365 Integration

Bosch Reveals AI Cockpit at CES 2026 with 200 TOPS Processing and Microsoft 365 Integration AMD Advocates Integrated AI Compute with EPYC CPUs for 50% Cost Savings and Enhanced Performance

AMD Advocates Integrated AI Compute with EPYC CPUs for 50% Cost Savings and Enhanced Performance AI Transforms Missile Guidance: Neural Networks Enhance Target Engagement and Adaptivity

AI Transforms Missile Guidance: Neural Networks Enhance Target Engagement and Adaptivity NASA Integrates AI in Artemis and VIPER Missions to Enhance Lunar Exploration and Data Processing

NASA Integrates AI in Artemis and VIPER Missions to Enhance Lunar Exploration and Data Processing