The AI arms race among Big Tech continues to escalate, with companies investing tens of billions of dollars into data centers, talent, and compute power to achieve the next significant advancements in reasoning, multimodality, and practical applications. For everyday investors, the stakes are personal: Will this extensive spending translate into revenue growth that justifies lofty valuations, or will delays and unmet benchmarks undermine market confidence?

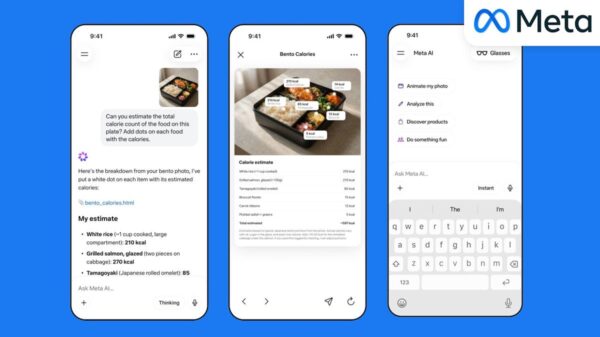

Meta Platforms (NASDAQ:META) recently provided a pertinent case study. Last week, the company launched Muse Spark, its first major AI model in over a year and the inaugural product from Meta Superintelligence Labs. The market reacted quickly, boosting Meta’s stock nearly 10% over the last five trading days, closing Friday at $629.86 per share.

Muse Spark did not release on its originally planned timeline. In March, Meta delayed the rollout of the model, previously codenamed Avocado, after internal tests indicated it did not meet performance benchmarks set by rivals. The company needed additional time to compete with models such as Google’s Gemini 3.0. Executives postponed the launch until at least May while reorganizing the AI team after the previous year’s disappointing Llama 4 release.

This delay raised concerns among investors, who feared that waiting could cede ground to quicker competitors like OpenAI, Anthropic, and Google DeepMind. The pace of innovation in the AI sector is rapid, with new capabilities emerging almost monthly. However, Meta opted for patience over an early launch, a decision that seems to have paid dividends.

Muse Spark now powers the Meta AI app and the meta.ai website, with future integrations planned for WhatsApp, Instagram, Facebook, Messenger, and AI glasses. This shift represents a deliberate move towards a closed-source model focused on delivering “personal superintelligence.”

So, how does Muse Spark perform? Independent benchmarks released alongside the launch indicate that it is a competitive, though not dominant, player. It registers a score of 52 on the Intelligence Index, trailing behind leaders like Gemini 3.1 Pro and GPT-5.4 (both scoring 57) and Claude Opus 4.6 (53). However, it excels in health-related tasks, scoring 42.8 on HealthBench Hard, as well as in multimodal reasoning, aligning with Meta’s consumer-centric ecosystem.

In a blog post from Meta Superintelligence Labs, the company highlighted its emphasis on efficiency and practical utility over mere benchmark superiority. The model features tool use, visual chain-of-thought, and multi-agent orchestration while remaining “small and fast by design.” Compared to Llama 4, the upgrade appears significant.

While Muse Spark still lags in abstract reasoning and coding tasks, the competitive gap has narrowed enough that everyday users on Meta’s platforms should notice smarter and faster responses. For retail investors, the crucial question is not whether Muse Spark outperforms every rival today, but whether it positions Meta Platforms as a credible contender while the company seeks to monetize AI through advertising, subscriptions, and API previews.

Wall Street quickly recognized the potential, with Meta’s stock surging 6.5% on the announcement day alone, outpacing the S&P 500’s 2.5% gain and the Nasdaq’s 2.8% rise. This momentum continued throughout the week, leading to the nearly 10% return investors have observed.

The underlying business metrics remain robust. Meta Platforms generated $201 billion in total revenue for full-year 2025, reflecting a 22% year-over-year increase. The trailing 12-month earnings are approximately $23.49 per share, supporting a forward price-to-earnings ratio around 18. This valuation appears reasonable compared to competitors still working to demonstrate the financial benefits of AI. Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) trades at 23x, facing tougher advertising headwinds, while Microsoft (NASDAQ:MSFT) carries a slightly higher multiple of 19.6x on its Azure-AI investments. Meta’s ad-driven model, now enhanced by improved AI recommendations, positions it favorably for sustained growth.

Muse Spark was worth the wait. The delay allowed Meta Platforms to introduce a model that narrows the competitive gap without prematurely pushing an underdeveloped product to market. For discerning investors, the 10% stock increase over five trading days reflects renewed confidence in Meta Platforms’ AI strategy. However, the competitive race is relentless. With 22% revenue growth, an attractive price-to-earnings ratio, and AI now integrated across 3.98 billion monthly users, Meta Platforms offers retail investors a compelling opportunity to benefit from AI advancements without venturing into high-risk, speculative plays. For existing shareholders, the data supports maintaining positions, while newcomers may find this week’s release a strong reason to consider adding exposure during any market pullbacks. Patience, it seems, has indeed paid off.

See also Germany”s National Team Prepares for World Cup Qualifiers with Disco Atmosphere

Germany”s National Team Prepares for World Cup Qualifiers with Disco Atmosphere 95% of AI Projects Fail in Companies According to MIT

95% of AI Projects Fail in Companies According to MIT AI in Food & Beverages Market to Surge from $11.08B to $263.80B by 2032

AI in Food & Beverages Market to Surge from $11.08B to $263.80B by 2032 Satya Nadella Supports OpenAI’s $100B Revenue Goal, Highlights AI Funding Needs

Satya Nadella Supports OpenAI’s $100B Revenue Goal, Highlights AI Funding Needs Wall Street Recovers from Early Loss as Nvidia Surges 1.8% Amid Market Volatility

Wall Street Recovers from Early Loss as Nvidia Surges 1.8% Amid Market Volatility