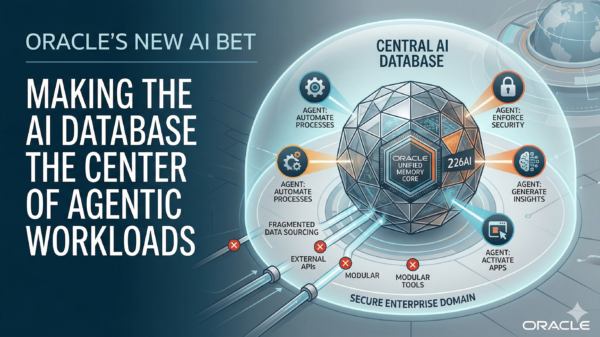

Everpure (PSTG) has launched its Evergreen//One for FlashBlade//EXA and a Data Stream beta, initiatives designed to address performance, scale, and data orchestration challenges in enterprise AI projects. These developments come amid a recent downturn for Everpure shares, which have seen a 19.82% decline over the past month and a 14.53% drop year-to-date. Despite this short-term volatility, total shareholder returns over three and five years remain robust, indicating a recent cooling of momentum following a strong multi-year performance.

The timing of these AI-focused product launches suggests a strategic pivot for Everpure, as the company seeks to enhance its position in the evolving AI infrastructure landscape. Current market conditions may prompt investors to reevaluate their perceptions of Everpure’s potential, especially given that the stock is trading below several valuation estimates. At its last close of $58.98, Everpure is perceived as materially undervalued relative to a fair value estimate of $91.00, signaling a significant gap based on specific growth and margin assumptions.

Analysts have set a consensus price target of $78.50 for Everpure, with expectations reflecting future earnings growth, profit margins, and associated risk factors. However, opinions among analysts vary, with the most optimistic targeting $93.00 and the most pessimistic placing the figure at $55.00. This divergence highlights the uncertainty surrounding Everpure’s growth trajectory and the assumptions that underpin its valuation.

The narrative suggesting Everpure’s undervaluation hinges on projections of accelerated earnings growth, steadier revenue streams, and improved profit margins compared to current market pricing. Nonetheless, this outlook is contingent on the company effectively managing increased research and development expenses and infrastructure investments, as well as avoiding prolonged margin pressure due to potential shortfalls in cloud transition, hyperscaler wins, or hardware demand.

While the fair value narrative paints a positive picture, Everpure’s current price-to-earnings (P/E) ratio of 103.6x starkly contrasts with the technology sector average of 20.5x and a fair ratio of 44.9x. This discrepancy may indicate elevated expectations from investors, raising questions about whether the market is underestimating Everpure’s growth potential or pricing in future performance too aggressively.

As the stock’s performance continues to be scrutinized, potential investors may find it worthwhile to examine the four key rewards associated with Everpure’s offerings and consider how these align with their investment goals. The current situation presents an opportunity for analysts and investors alike to assess the underlying factors influencing Everpure’s valuation and performance in the competitive AI landscape.

In conclusion, the recent product launches by Everpure are a strategic response to the challenges faced in the enterprise AI sector, an area characterized by rapid growth and significant investment. With its shares under pressure but still showing strong long-term returns, the company appears at a crossroads. Investors will need to weigh the risks and opportunities presented by Everpure’s new initiatives, as well as their implications for future growth in a complex and evolving market.

See also Bank of America Warns of Wage Concerns Amid AI Spending Surge

Bank of America Warns of Wage Concerns Amid AI Spending Surge OpenAI Restructures Amid Record Losses, Eyes 2030 Vision

OpenAI Restructures Amid Record Losses, Eyes 2030 Vision Global Spending on AI Data Centers Surpasses Oil Investments in 2025

Global Spending on AI Data Centers Surpasses Oil Investments in 2025 Rigetti CEO Signals Caution with $11 Million Stock Sale Amid Quantum Surge

Rigetti CEO Signals Caution with $11 Million Stock Sale Amid Quantum Surge Investors Must Adapt to New Multipolar World Dynamics

Investors Must Adapt to New Multipolar World Dynamics