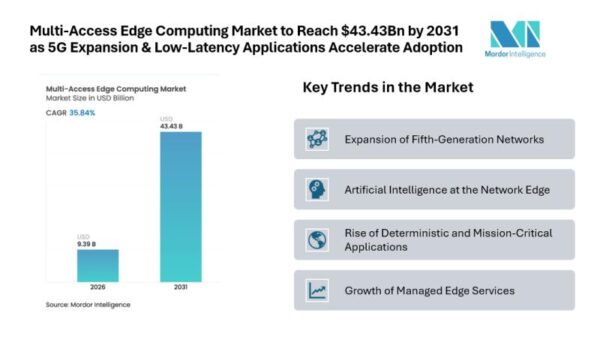

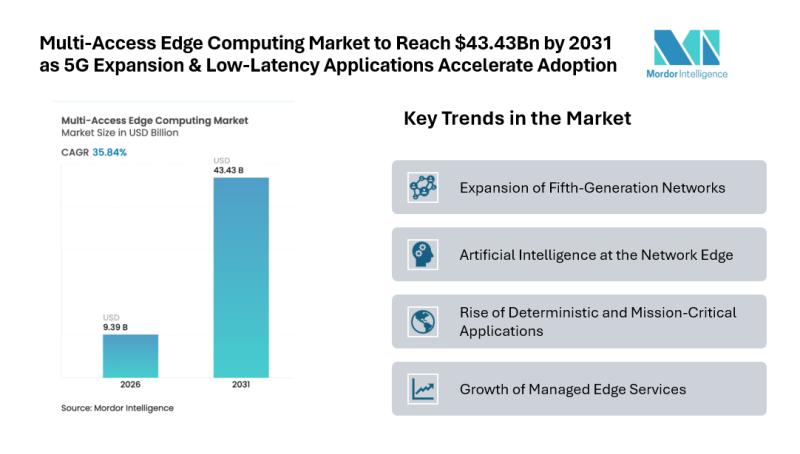

Mordor Intelligence has released a report detailing the growth trajectory of the multi-access edge computing (MEC) market, projecting an increase from USD 6.91 billion in 2025 to USD 9.39 billion in 2026, ultimately reaching USD 43.43 billion by 2031. This represents a compound annual growth rate (CAGR) of 35.84% during the forecast period. The analysis underscores a significant shift from centralized cloud processing to distributed infrastructures capable of delivering real-time performance, vital for modern applications that cannot afford latency stemming from distant data centers.

Industries such as manufacturing, transportation, healthcare, retail, and smart cities are fueling demand for instant analytics and automation, necessitating immediate data processing capabilities. By situating compute, storage, and networking resources at the network edge, organizations can achieve data processing within milliseconds of its creation. This capability is increasingly critical for applications reliant on artificial intelligence (AI) inference, immersive experiences, and mission-critical operations. The report notes that the MEC sector is being further stimulated by the widespread deployment of standalone fifth-generation networks, as telecom operators integrate edge nodes into their infrastructure to enable new services and enterprise functionalities.

While hardware investment in MEC remains substantial, there is a noticeable shift toward managed services. Many companies are opting to outsource the complexity associated with deployment, reflecting a broader trend in the market. The growth of multi-access edge computing indicates a long-term structural change in the way digital services are delivered, fundamentally altering business models across sectors.

The report identifies several key trends driving this market. One prominent factor is the expansion of fifth-generation networks, which is bolstering MEC capabilities. Telecom providers are deploying edge infrastructure in tandem with base stations, facilitating ultra-low latency services critical for applications like real-time video processing and smart infrastructure. As coverage improves, enterprises stand to benefit from enhanced high-speed connectivity, further solidifying telecom-led deployments’ roles in the MEC market.

Moreover, businesses are increasingly running AI workloads closer to data sources, allowing for faster decision-making and reduced bandwidth consumption. This edge-based AI model also enhances privacy, making it integral for use cases such as predictive maintenance, intelligent surveillance, and personalized retail experiences. As organizations adapt to this paradigm, the MEC market experiences substantial growth, largely due to the urgent need for real-time processing in various AI applications.

Another significant trend is the rise of deterministic and mission-critical applications. Industries with sensitive systems necessitate reliable performance with minimal delay, making robotics, remote control systems, and industrial automation prime candidates for MEC adoption. Edge computing environments provide the reliability and speed essential for these applications, and as enterprises modernize their operations, this segment of the MEC industry is seeing increased uptake.

A growing preference for managed edge services is also reshaping the competitive landscape. While some organizations choose to establish their own infrastructure, many are turning to telecom operators, cloud providers, or system integrators for managed solutions. This choice allows for reduced operational complexity and upfront investment, while ensuring ongoing maintenance and security, thereby expanding participation within the MEC ecosystem.

The report further categorizes the MEC market based on components, deployment models, applications, end-user verticals, and geography. Key players identified include major firms such as Microsoft Corporation, Hewlett Packard Enterprise Company, Dell Technologies Inc., NVIDIA Corporation, and Akamai Technologies, Inc.

As the multi-access edge computing market transitions from early adoption to mainstream deployment, the demand for instant responsiveness in digital services is more pronounced than ever. This shift allows organizations to unlock capabilities that traditional cloud architectures cannot provide. While the momentum is strong, challenges remain, such as high capital requirements for infrastructure deployment, concerns regarding data security at distributed locales, and the lack of standardized orchestration frameworks. However, ongoing collaborations among industry stakeholders are beginning to address these issues, with partnerships between telecom operators, cloud providers, and technology vendors fostering interoperable ecosystems to support large-scale rollouts.

The long-term outlook for the MEC market across various industries remains highly favorable. With initiatives dependent on localized processing capabilities, such as real-time analytics and autonomous systems, the demand for edge solutions is poised to accelerate. As applications progress from pilot stages to full production, the multi-access edge computing industry is set to play a foundational role in the next generation of digital services. Continued investments in network infrastructure and AI integration will sustain the momentum of market growth in the coming years, offering early adopters significant advantages in performance and operational efficiency.

See also Affordable Android Smartwatches That Offer Great Value and Features

Affordable Android Smartwatches That Offer Great Value and Features Russia”s AIDOL Robot Stumbles During Debut in Moscow

Russia”s AIDOL Robot Stumbles During Debut in Moscow AI Technology Revolutionizes Meat Processing at Cargill Slaughterhouse

AI Technology Revolutionizes Meat Processing at Cargill Slaughterhouse Seagate Unveils Exos 4U100: 3.2PB AI-Ready Storage with Advanced HAMR Tech

Seagate Unveils Exos 4U100: 3.2PB AI-Ready Storage with Advanced HAMR Tech