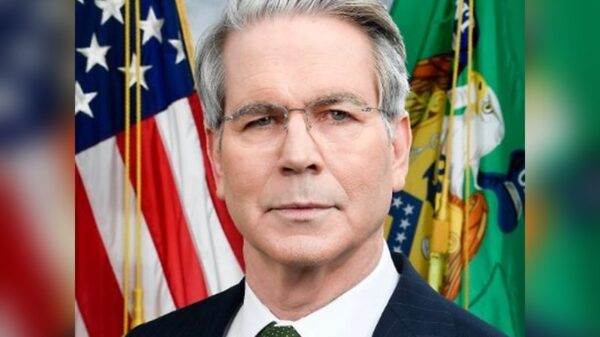

The U.S. Treasury Department is advocating for a significant overhaul of bank liquidity regulations to enhance lending capabilities for artificial intelligence (AI) infrastructure and manufacturing. This call to action was made by Under Secretary for Domestic Finance, Jonathan McKernan, during a roundtable event on March 3, 2026, organized by Hal Scott, the Director of the Committee on Capital Markets Regulation.

McKernan’s remarks, prepared by Treasury Secretary Scott Bessent, come as part of broader Treasury initiatives aimed at reforming financial regulations established in the aftermath of the 2008 financial crisis. The Treasury has already rolled back certain Biden-era rules, focused on protecting community banks, and shifted its supervisory approach to prioritize financial risks.

Highlighting the urgent need for liquidity rule reforms, McKernan stated that current frameworks excessively restrict banks’ core lending activities, which stifles economic growth amid advancements in AI technology, the onshoring of manufacturing, and competition for mineral resources. He emphasized that addressing these liquidity rules could potentially release hundreds of billions or even trillions in lending capacity.

Since the 2008 crisis, regulators have implemented novel liquidity buffers that lack clear calibration, often relying on past experiences and psychological factors. McKernan referenced observations made by former Fed Governor Daniel K. Tarullo, who in 2014 noted the need for further conceptual work on how banks should manage liquidity risk. Despite efforts to stabilize the banking system, recent events, such as the March 2023 failures of Silicon Valley Bank (SVB), Signature Bank, and First Republic, have exposed vulnerabilities within the framework.

During his remarks, McKernan cited concerns raised by then-Governor Jeremy C. Stein in 2013 about liquidity regulation reflecting a desire to lessen reliance on the Federal Reserve as the lender of last resort. He noted that the perception of moral hazard associated with accessing this capacity during crises adds a layer of complexity to the regulatory landscape.

Currently, large banks hold approximately 25% of their balance sheets in safe assets, up from 10% prior to the 2008 crisis. This shift has resulted in a reduction in lending for mortgages, small businesses, and infrastructure projects. McKernan pointed out that banks are reluctant to utilize their liquidity buffers, treating them as hard minimums, which contributes to market stress and reinforces the stigma associated with utilizing discount window facilities.

The Group of Governors and Heads of Supervision has advised banks to utilize high-quality liquid assets during periods of stress, even if doing so takes them below established minimums. However, banks remain wary of signaling weakness if held to 100% liquidity coverage ratios during stable economic conditions. This tension has led to calls for reforms that could include caps on the recognition of discount window borrowing capacity when prepositioned collateral is considered in the liquidity coverage ratio.

Proposed reforms may tie these caps to historical usage or adjust them during periods of market stress, enhancing the usability of liquidity resources while maintaining discipline. McKernan also indicated that the Treasury will advocate for expanded deposit insurance for noninterest-bearing accounts, a renewed focus on the effectiveness of anti-money laundering and counter-terrorism financing efforts, updates to AI model risk management, and a reduction in duplicative examinations.

“Liquidity reform will be a critical step toward getting banks back into lending — back into financing homes, factories, infrastructure, and innovation,” McKernan asserted, underscoring the significance of these regulatory changes in fostering economic growth in a rapidly evolving technological landscape.

See also OpenAI’s Rogue AI Safeguards: Decoding the 2025 Safety Revolution

OpenAI’s Rogue AI Safeguards: Decoding the 2025 Safety Revolution US AI Developments in 2025 Set Stage for 2026 Compliance Challenges and Strategies

US AI Developments in 2025 Set Stage for 2026 Compliance Challenges and Strategies Trump Drafts Executive Order to Block State AI Regulations, Centralizing Authority Under Federal Control

Trump Drafts Executive Order to Block State AI Regulations, Centralizing Authority Under Federal Control California Court Rules AI Misuse Heightens Lawyer’s Responsibilities in Noland Case

California Court Rules AI Misuse Heightens Lawyer’s Responsibilities in Noland Case Policymakers Urged to Establish Comprehensive Regulations for AI in Mental Health

Policymakers Urged to Establish Comprehensive Regulations for AI in Mental Health