The semiconductor industry is set to enter 2026 with a renewed sense of momentum, driven largely by the rise of artificial intelligence (AI) and a wave of strategic acquisitions. Following a tumultuous post-pandemic period marked by significant inventory corrections and fluctuating demand, AI has emerged as a critical growth driver, prompting substantial investments across advanced logic, memory, and data center infrastructure.

Major players in the industry are increasingly turning to acquisitions to bolster their competitive positions. Texas Instruments (TI) recently announced its plan to acquire Silicon Labs for $231 per share, alongside approximately $7 billion in incremental debt. This acquisition, awaiting regulatory approval, is expected to close in early 2027 and will expand TI’s embedded wireless connectivity portfolio significantly. The deal will add 1,200 new products and an extensive suite of software, firmware, and applications, essential components that are challenging to replicate in a fast-evolving market where top engineering talent is heavily focused on AI data center initiatives.

As the semiconductor sector moves into 2026, projections remain optimistic. Deloitte forecasts global chip sales will soar to $975 billion, with year-over-year growth accelerating from 22% to 26%. However, this growth is notably concentrated; chips designed for generative AI are anticipated to account for approximately $500 billion, representing over half of the industry’s total revenue despite making up less than 0.2% of total unit volume. Deloitte estimates that just 20 million of the 1.05 trillion chips sold in 2025 were intended for generative AI applications.

This high-margin, low-volume model has disturbed traditional market dynamics as major chipmakers pivot toward lucrative AI chips, leaving non-AI semiconductor buyers grappling with dwindling inventory levels and rising prices. The overwhelming share of AI-related revenue also raises concerns about the industry’s overall stability, as it becomes increasingly tethered to a narrow set of AI-oriented roadmaps. Deloitte warns that delays in monetization or bottlenecks in data center expansions could negatively affect the entire sector, even as many non-AI segments may face slower growth or declines in 2026.

Memory products represent a significant stress point in this evolving landscape. Deloitte projects memory revenue to reach $200 billion in 2026, yet suppliers remain cautious about expanding capacity for lower-margin products. This figure is expected to skew heavily toward high-priced memory solutions for AI hyperscalers, with AI’s insatiable demand for High Bandwidth Memory (HBM) likely pushing up prices for DDR4 and DDR5 memory.

The impact of AI extends beyond mere financial figures, influencing the demand tied to data center expansions and the specialized networking and power ecosystems required to support them. This necessitates sustained capital expenditures in areas such as advanced packaging and power/thermal management, crucial factors that will determine the pace at which new AI facilities can be deployed. In contrast, the consumer electronics sector, having experienced its own challenges, is seeing a normalization that may help stabilize the supply-demand balance, but AI remains the primary growth catalyst.

For supply chain leaders, the shift toward “normalization” in the chip industry does not imply a return to previous cycles. Instead, the AI-led environment introduces new risks related to allocation and pricing volatility. The consolidation movement seen with TI’s acquisition of Silicon Labs exemplifies a broader trend as major players seek to vertically integrate and streamline their offerings. While such strategies can simplify procurement for customers, they also result in diminished supplier diversity, creating vulnerabilities in the face of potential disruptions.

Looking ahead, semiconductor firms will need to adopt disciplined sourcing strategies as they navigate this new landscape. Early qualification of alternatives, tracking lifecycle transitions, and maintaining flexibility across geographic and channel dimensions will be crucial in mitigating risks associated with single-source dependencies. Sourceability, with over a decade of experience, aims to assist customers in securing early allocations in high-growth categories while diversifying sourcing to reduce exposure to price fluctuations and demand disruptions.

See also AI Expert Warns of Psychosis Signs in 560K Users Amid Concerns Over Chatbot Design

AI Expert Warns of Psychosis Signs in 560K Users Amid Concerns Over Chatbot Design Multiverse Computing Launches Free HyperNova 60B AI Model with 32GB Footprint

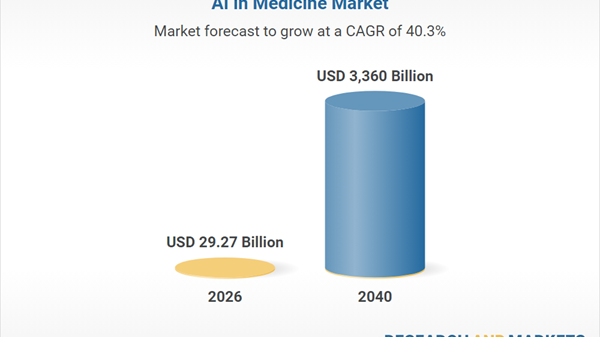

Multiverse Computing Launches Free HyperNova 60B AI Model with 32GB Footprint Vector-Borne Disease Surveillance AI Market to Reach $4.01 Billion by 2030 with 20.2% CAGR

Vector-Borne Disease Surveillance AI Market to Reach $4.01 Billion by 2030 with 20.2% CAGR TD SYNNEX Partners with SCAILIUM for AI Infrastructure, Boosting Growth Potential

TD SYNNEX Partners with SCAILIUM for AI Infrastructure, Boosting Growth Potential SambaNova Secures $350M and Partners with Intel to Develop Next-Gen AI Chips

SambaNova Secures $350M and Partners with Intel to Develop Next-Gen AI Chips