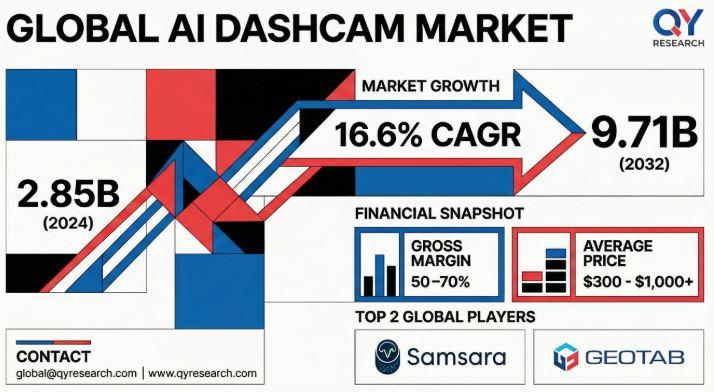

The market for AI dashcams is poised for significant growth, evolving from basic video recording devices into sophisticated, AI-driven risk management tools. According to recent research, the sector is expected to expand from USD 2.85 billion in 2024 to USD 9.71 billion by 2032, achieving a compound annual growth rate (CAGR) of 16.6%. This growth is increasingly fueled not by hardware sales, but by subscription-based video telematics and AI-powered safety analytics, marking a shift from low-margin device sales to higher-margin software-as-a-service (SaaS) with stable, recurring revenue streams.

AI dashcams differentiate themselves within mobility ecosystems by producing visual, legally admissible data that traditional telematics cannot provide. They also enable monetization opportunities post-incident, such as insurance claims and legal defense, a capability that advanced driver-assistance systems (ADAS) lack. Unlike generic IoT sensors, AI dashcams offer quantifiable financial returns through reductions in accidents and expedited claims processing. The implication is clear: these devices are not mere hardware; they serve as risk intelligence platforms that deliver direct economic benefits.

Market dynamics reveal a varied commercialization landscape. Consumer devices constitute approximately 60% of unit volume but yield lower margins. In contrast, enterprise adoption focuses on digitization, necessitating hardware upgrades and system integration. Revenues often remain tied to basic recording capability rather than advanced AI analytics. Current market positioning indicates an inflection point where high-value growth is increasingly directed toward enterprise fleets as AI functionalities mature.

However, several critical misconceptions cloud the market’s opportunity assessment. AI dashcams are often misclassified as consumer electronics, with their true value lying in advanced AI models and SaaS platforms. While demand is primarily driven by fleet operators, insurers are also major contributors, promoting adoption through premium incentives. Short-term growth faces challenges from regulatory and integration barriers, yet the long-term potential is often underestimated as AI video technology becomes foundational for autonomous datasets and liability frameworks. A revised valuation approach is essential, treating these products as integrated SaaS and data infrastructure rather than mere commodity hardware.

The economic model for AI dashcams shows promising scalability. Hardware costs range from $300 to over $1,000 per vehicle, accompanied by monthly SaaS subscription fees between $30 and $70. This structure offers payback periods of six to 12 months through lowered insurance premiums and diminished accident rates, fostering high returns on investment and exceptional customer retention. The market is fundamentally driven by risk mitigation, particularly among fleet operators, logistics companies, and ride-hailing services, where safety is paramount.

In terms of regional dynamics, North America leads the market with more than 36% share, driven by aggressive fleet digitization and insurance incentives. The Asia-Pacific region is projected as the fastest-growing area, propelled by high vehicle density and government mandates for improved safety in countries like China and India. Europe presents a more complex growth environment, constrained by GDPR and stringent data privacy regulations. Consequently, while growth appears global, it is intricately shaped by local regulations and insurance frameworks.

The supply chain for AI dashcams is transforming, moving from basic camera assembly to a complex ecosystem encompassing hardware, software, and AI capabilities. Leading manufacturers specializing in vision-based AI and cloud telematics achieve gross margins of 50% to 70%, thanks to proprietary computer vision algorithms and edge-processing technologies. Value is increasingly concentrated in three layers: hardware and optical integrators, edge intelligence and system-on-chip (SoC) providers, and high-margin SaaS and analytics platforms. Companies such as Samsara and Motive capture ongoing value through subscription models that integrate video data into various workflows.

Asia-Pacific is emerging as a pivotal production hub, with countries like China and Taiwan leading in hardware manufacturing, leveraging established semiconductor networks. Innovations such as edge-side behavior coaching and privacy-first masking algorithms are enhancing AI dashcam functionalities. The latest technological advancements also include low-power modes that allow cameras to utilize minimal energy while maintaining readiness to capture critical incidents.

Overall, the AI dashcam sector is at the forefront of a transformative shift from passive recording to proactive risk management and safety monetization. The success of market players will depend on their ability to control AI software and data layers, integrating these systems within the broader insurance and fleet management workflows to deliver measurable financial impact. As the technology continues to evolve, AI dashcams are set to become foundational elements of the connected vehicle ecosystem, influencing the future landscape of mobility and safety.

See also Kyndryl Empowers 50% of Staff to Create AI Agents, Boosting Productivity and Workflows

Kyndryl Empowers 50% of Staff to Create AI Agents, Boosting Productivity and Workflows Generative AI Enhances Health Care Efficiency, Transforming Industry Operations

Generative AI Enhances Health Care Efficiency, Transforming Industry Operations Egoras and Airtel Launch AI-Powered Cube Phone with Zero-Cost Connectivity for Businesses

Egoras and Airtel Launch AI-Powered Cube Phone with Zero-Cost Connectivity for Businesses Obriy AI Secures $500K to Scale SURE Legal Automation Platform in Ukraine

Obriy AI Secures $500K to Scale SURE Legal Automation Platform in Ukraine Enterprise Architecture Shifts to Customer Journey Focus, Boosting Revenue Retention

Enterprise Architecture Shifts to Customer Journey Focus, Boosting Revenue Retention