Shares of Vertiv (VRT) have surged over 250% in the past year, reflecting strong investor confidence in the company’s critical role in powering and cooling AI data centers. This impressive performance has elevated Vertiv’s stock to approximately 47 times forward earnings, a notable multiple for an industrial firm of its kind. The uptick in stock value comes on the heels of the company’s first-quarter adjusted earnings report, which revealed an 83% year-over-year growth, driven by a project backlog that has more than doubled to exceed $15 billion.

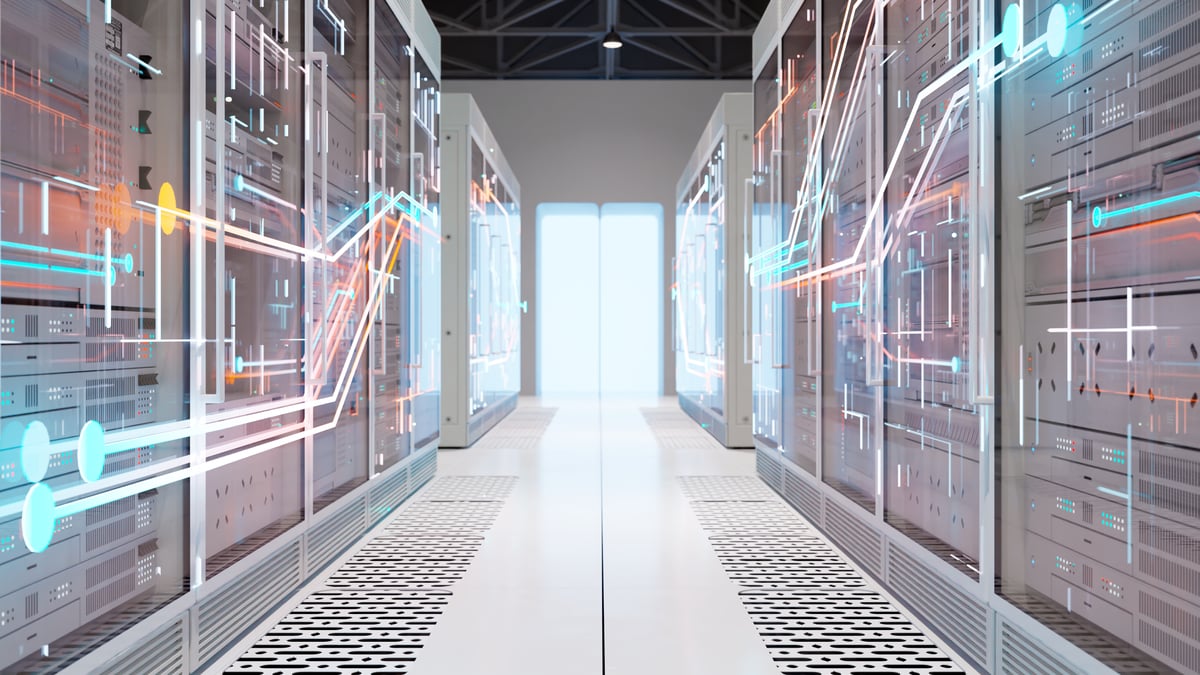

The demand for Vertiv’s offerings is largely attributed to the rapid transition toward high-density AI racks, which necessitate advanced liquid-cooling systems that the company specializes in. As AI workloads increasingly drive higher rack power densities, liquid cooling is becoming the primary thermal solution for the most power-hungry compute rows. This new liquid-cooled infrastructure operates in conjunction with traditional air-cooled systems, which still serve the broader data center environment.

Many of the recent AI deployments leverage direct-to-chip liquid cooling technology, where fluid circulates through cold plates affixed to high-performance chips to effectively dissipate heat. Vertiv’s solutions contribute to significant energy savings, with some systems boasting a reduction in annual cooling energy consumption by up to 70%. The company delivers a comprehensive range of products, including coolant distribution units, pumps, and heat rejection systems, thereby enhancing the overall value it provides per rack. This demand has fueled an impressive 44% organic sales growth in its Americas segment during the first quarter, primarily due to significant investments from U.S. hyperscale data centers.

Vertiv’s strategic collaborations with silicon partners like Nvidia provide the company with insights into the evolving technical requirements for future deployments. With a robust backlog valued at $15 billion, Vertiv is positioned for a stable revenue stream over the next 12 to 18 months, reducing short-term cyclical risks. The conversion of larger, more complex projects has resulted in incremental margins exceeding 30%, reflecting positively in the company’s financial performance. In the first quarter, adjusted operating margins expanded by 430 basis points to reach 20.8%, which bolstered Vertiv’s optimistic forecast of 30% organic growth and 51% earnings growth by 2026.

While the impressive cash flow enables further capacity expansion to meet demand, it also serves as a buffer against the ongoing challenges in the EMEA segment, where organic sales declined by 29% in the recent quarter. Management anticipates a recovery in that area during the latter half of the year, but the primary growth driver remains the escalating need for infrastructure in the Americas.

Despite concerns about a stretched valuation, the fundamental requirements of purpose-built data centers and the sheer scale of spending in the sector underpin a durable demand for Vertiv’s solutions. Investors with a long-term outlook, particularly those interested in AI infrastructure, may find Vertiv to be a compelling addition to their portfolios. The company’s ability to adapt to the rapid evolution of technology, coupled with its extensive project pipeline, positions it well for sustained growth in a landscape increasingly dictated by AI advancements.

See also Galaxy Digital Shifts Focus to AI Data Centers, Reports $216M Q1 Loss

Galaxy Digital Shifts Focus to AI Data Centers, Reports $216M Q1 Loss Nebius Acquires Eigen AI for $643M to Enhance AI Infrastructure and Efficiency

Nebius Acquires Eigen AI for $643M to Enhance AI Infrastructure and Efficiency New York City Cancels AI-Focused High School Amid Widespread Parental Backlash

New York City Cancels AI-Focused High School Amid Widespread Parental Backlash Apple Faces Mac Mini and Studio Shortage as OpenClaw Drives AI Demand Surge

Apple Faces Mac Mini and Studio Shortage as OpenClaw Drives AI Demand Surge Silicon Wafer Shipments Surge 13% in Q1 2026, Driven by AI Data Center Demand

Silicon Wafer Shipments Surge 13% in Q1 2026, Driven by AI Data Center Demand